It’s Tax Season! Here is What Employers Need to Know About the IRS’s Affordable Care Act Reporting Requirements (with Deadlines)

In February 2015, the IRS issued final forms and instructions related to the Affordable Care Act (ACA). Back in December, 2015, the IRS issued a deadline extension for the new ACA reporting requirements. For tax year 2015, employers and insurance carriers are required to report medical coverage data under Internal Revenue Code sections 6056 and 6055.

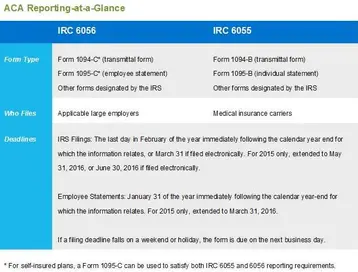

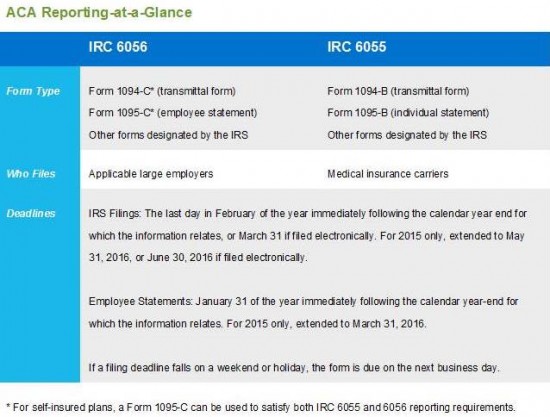

Below is what you need to know to decide what you need to report and what form to use. The chart above is a handy reminder of the deadlines to file this paperwork.

Start by figuring out if your company is considered an applicable large employer (ALE)

An ALE is a company that employed 50 or more full-time employees, including full-time equivalent employees (FTEs), on average during the previous calendar year. Generally, a full-time employee is someone who works 30 or more hours a week, on average. Internal Revenue Code section 6056 applies to companies that meet the definition of an ALE, including companies that did not offer group medical coverage in 2015.

TriNet encourages all companies that fall into this category to brush up on our previous information about ALEs and their ACA reporting requirements.

It is important to note that the IRS will impose penalties on ALEs that fail to make a good faith effort to furnish the forms in 2016, which will report offers of coverage in 2015. Failure to do so results in a penalty of $100 per statement, up to $1.5 million each calendar year—unless the ALE intentionally disregards the requirement. In that case, there is no maximum penalty.

It is important to note that the IRS allows an ALE to use a third party to help with the preparation of the reports. TriNet, for example, offers ACA reporting assistance to our clients.

ALE reporting responsibilities to employees

Once you’ve figured out that you are an ALE, your first concern should be in sending to all your full-time employees – and to the IRS - information about the medical coverage, if any, your company offered in 2015. All ALEs are required to report 2015 coverage information in early 2016 (see chart above for specific deadlines), including ALEs with 50-99 FTEs who qualify for ACA employer shared responsibility transition relief for 2015.

ALEs must provide IRS form 1095-C to each full-time employee who was employed during the 2015 calendar year. This form is required to help the IRS determine employee eligibility for premium tax credits if the employer does not offer affordable and compliant health coverage as defined by the ACA.

The form 1095-C includes the ALE’s name, address and employer identification number (EIN) and the ALE’s contact person, as well as:

- The name, address and taxpayer ID number (usually the social security number) of the full-time employee and months during which the employee was covered under an eligible employer-sponsored plan

- The months during the calendar year in which minimum essential coverage (MEC) was available to the full-time employee

- The share of the lowest cost monthly premium for employee-only coverage providing minimum value offered to full-time employees under an eligible employer-sponsored plan.

- If a plan is self-insured, information about coverage dependents.

What defines minimum essential coverage (MEC)?

MEC includes employer-sponsored medical plans, as well as coverage under government-sponsored plans, individual market plans and other types of coverage recognized by the U.S Department of Health & Human Services. All TriNet medical plans are MEC.

IRS filing for ALEs

ALEs must also submit the coverage data included on the 1095-C statements to the IRS, along with form 1094-C, which needs to include:

- The name, address and employer identification number (EIN) of the ALE, and the name and telephone number of the ALE’s contact person

- Certification for each calendar month that the ALE offered full-time employees and their dependents the opportunity to enroll in MEC under an eligible employer-sponsored plan

- The number of full-time employees for each month during the calendar year

- The number of employee statements being submitted

- If applicable, the names and EINs of companies that are members of the aggregated ALE group (controlled group).

Internal Revenue Code section 6055 reporting requirements

This rule requires all organizations that provide MEC to report health care coverage to the IRS and provide a statement to all covered individuals. The entities that must comply with internal revenue code 6055 include:

- Health insurance issuers

- Self-insured health plan sponsors

- Government agencies that administer government-sponsored health insurance programs

- Any other entity that issues MEC.

For instance, if a medical plan is fully insured, the insurance carrier is responsible for filing the applicable section 6055 reports to the IRS and distributing statements to covered employees.

This information that must be reported to the IRS using form 1095-B (or 1095-C in certain instances), which includes:

- The name, address and employer identification number (EIN) of the entity required to file the form (e.g., the health insurance carrier)

- The name, address and taxpayer ID number (usually the Social Security number) of each individual covered under the medical plan, including eligible dependents

- The months for which the individual was enrolled in coverage and eligible to receive benefits for at least one day during the month

These rules don’t apply to supplemental health plans, such as a health savings accounts or health reimbursement accounts.

How should ALEs distribute statements to employees?

Under both sections 6056 and 6055, employee statements may be distributed electronically or via paper. However, to distribute electronically, employees must consent to receiving electronic delivery.

Still confused?

Many small businesses are following the ever-changing regulations of ACA and are still struggling with how to maintain compliance, especially with the new reporting requirements. TriNet spends our time closely monitoring the ACA so you don’t have to. We have the resources and expertise to take much of the burden off employers. Contact us for more information about staying compliant with ACA rules and regulations.

Handling HR and Compliance on Your Own?

Answer a few quick questions to see which HR solution fits your business.

Trending now

- HR Essentials, HR Outsourcing

- HR Outsourcing, HR Technology

- HR Essentials, HR Outsourcing

Get Help Navigating HR Compliance

Our experts can help you stay on top of HR rules and requirements so you can focus on running your business with confidence. Reach out. We're here to help.